Innovation vs. Focus and Scale

Enjoy this letter penned by Kyle Benusa speaking about his and Jack Allen’s experience following a thought provoking session at our Spring Retreat.

Contributed by Kyle Benusa of Ballast Consulting Group

Jack and I attended a lecture of sorts a few weeks back and the speaker spent a lot of his time on the topic of neuroplasticity. The overarching idea was that as we age, we get locked into mindsets, we get uncomfortable with unknowns and new ideas. The speaker argued that this provided an opportunity for those willing to put in the work. He encouraged us to seek new experiences and get exposure to new ideas often. Our return on this investment would be agility, speed, and innovation. Sexy stuff.

Following the lecture, Jack and I walked back to our cottage in silence. If you know us, you know that’s an atypical scene. We’re typically opinionated, overly confident, comfortable enough with each other that we’re usually talking OVER each other.

Once we got back to the cottage and got settled in, we launched into deep debate. Debating is our preferred method of working through ideas. He will take one side; I’ll take the other. We position, pivot, reposition until we’ve beaten the damn idea up so badly, we can walk out of the conversation feeling confident in a path. We have a bias for action, and this method proves faster than other approaches at working through the brain fog that accompanies learning new frameworks and ideas. This brain fog is like dust and dirt getting kicked up as new ideas collide with old beliefs and your brain tries to work towards some kind of reconciliation.

This time was a little different. It was harder for us to get clarity through debate. It was easier for both of us to take both sides of the argument. We walked away without clearing the dust or fog. We just got comfortable living in it.

Now that we’ve had a little while to think and process, we wanted to write a Ballast letter on it, hoping it would help me process the ideas further, maybe provide a little more clarity.

The dust-up: innovation vs focus & scale

The two competing ideas engaged in this dust up are: innovation versus focus & scale.

- Innovation is launching a new service line or product, testing a new pricing model, going after a new industry. It’s how we evolve. It’s the spark.

- Focus & scale is streamlining delivery, doubling down on what works, tightening the playbook. It’s how we drive margin, build repeatability, and create operational power. It’s the engine.

In a world of unlimited capital and resources, I suppose these two ideas don’t necessarily have to compete, but in our business (and in most of our clients’ businesses) these two ideas most certainly do compete. Every dollar and every hour we spend on one is a dollar and hour made unavailable for the other.

But it’s more than that isn’t it? The conflict between these two ideas or concepts is greater than the limited-resource argument. People and processes that desire innovation feel weighed down and held back by the people and processes built to focus, standardize, and scale.

On the other side of this metaphorical showdown are the scalers, the people and processes that desire focus and scale. These people feel distracted by those who are always pushing for innovation. The innovators come across as ‘seagulls’ just dropping in from time to time with their distractions. At Ballast, we express this frustration by claiming that the innovative ideas are like throwing sand in the gears of this machine we’ve built. We make money as a firm, for our employees, for our growth, when the machine is humming. Can we please stop stopping the machine from spinning to tinker on this cog or that driveshaft?

And so I hold the two following thoughts in my head at the same time:

- Innovation in a business is needed and has tremendous value, yet

- Focus and standardization are a prerequisite for scale, and success requires some scale.

And these ideas are in tension, they are in friction. They fight. But I’m still holding both in my head and I haven’t gone entirely mad just yet

Let’s dig into the two concepts and let this epic business scuffle play out.

Innovation

We all know the folksy business tropes about successful businesses that fail to innovate, that fail to adapt and change and, because of this failure, eventually decline. Growing up we learn about major declines – the Roman Empire, the British Empire, etc. As we dip our toes into the business world, we learn about Kodak, US Steel, and Blockbuster. We read Jim Collins’ How the Mighty Fall.

And that scares us. The idea of turning around one day and realizing that the business you built has been passed over and now holds little to no power or influence. Yikes. As entrepreneurs we’ve poured our hearts and souls into our businesses, so the idea of them withering away is upsetting.

And maybe this isn’t just an emotional reaction. Maybe it should scare us. These historical narratives are not wrong or untrue. And because of this, burned within our brains is the fundamental belief that innovation is good for business. It’s a must. It’s a requirement. Innovation results in wins and success. If you want to avoid that slow and embarrassing decline into nothingness, innovate. Without it, we atrophy. Without it, markets fail. And by god it’s incumbent on us to be the ones to innovate.

Focus and Scale

Scale has power and force and magnitude. Scale brings efficiency and higher quality. And in business we’ve all learned these lessons as well. We read Gladwell’s Outliers, we understand the idea of investing 10,000 hours into something with singular focus in order to become great. We’ve all read about Henry Ford’s assembly line and the intense focus on the production of a single vehicle. This focus allowed for extraordinary gains in efficiency, allowing Ford to reduce the sales price of a Model T by 60% over the 19 years of production.

Later in business school, or amongst our roundtables or forums, someone eventually recommends Liker’s The Toyota Way and we learn the lessons of Toyota’s production system. Just look at numbers 6 and 8 of the 14 management principles outlined by Liker in his book:

- Standardized tasks and processes are the foundation for continuous improvement and employee empowerment, and

- Use only reliable, thoroughly tested technology that serves your people and processes.

And it’s not just automobile production where this lesson teaches us about focus. Look at Southwest Airlines’ dedication to a single aircraft, the Boeing 737. This focus allowed them to streamline all of their operations. Mechanics, interior repairs, pilots, and on and on.

Or I’m sure you’ve read all about this guy named Steve Jobs (joking of course), who returned to Apple after being ousted, and he turned the business around by cutting down the product line by 70% and focusing on only a few key products. I don’t think a week goes by where I don’t see some jabroni on LinkedIn post that interview with Jobs where he talks about the need for simplicity.

And why and how does focus produce success? Ask our colleague John Reed over breakfast and by dinner he might take a breath. Two immediate things come to mind on why focus produces success:

- Higher volumes allow for more investment in fixturing and tooling, allowing for improved efficiency in production and reduced costs over time. These reduced costs can either produce higher margins (yay!) or allow for price reductions to improve competitive positioning.

- Standardized production allows for easier quality inspection, and higher volumes allow for the incorporation of quality assurance into the entire production line.

So focus produces higher quality products, at lower costs and/or higher margins. What’s not to love? And so a part of our business brain is hardwired to respect, appreciate, and desire focus, and scale, and standardization, and all of the wonderful things that come with it.

So…can we have both? Is there a reconciliation?

So how do we reconcile these two concepts? I really do wish we had a silver bullet, but this isn’t that kind of Ballast letter. We admit that we struggle with the competition between these two ideas at our firm. Every week I come up with something new I want to do, every week the team tells me to calm down and focus on our core.

I truly do not know the answer to how best to manage this conflict, but during our debate, Jack and I came up with a list of potential approaches:

1. Monogamous Approach

The idea behind this approach is that you choose either Focus OR Innovation, and you simply stay on your chosen path. The key here is to become exceptionally good at the path you’ve chosen, and become comfortable with or able to mitigate against the downside of NOT having the opportunity to engage with the other.

If you choose the path of focus, you can’t simply be okay at it, you must become relentless in your pursuit of it. Standardization and process are key. You must become good at understanding how to invest in the fixturing and tooling of your processes and the idea of investing in something for the sole purpose of reducing time and improving quality, and recouping this investment as quickly as possible.

The path of focus is not a flashy path. If you choose this path you have to become comfortable not doing anything new. And strategically, this means that in order to deepen the moat around your business, to keep the competitors at bay, you have to focus on cost and quality. The cost comment here might surprise you, but consider if you use your scale and position to drive so much efficiency and you share this efficiency with your customers and clients via price reductions (a la early Ford) that new entrants simply cannot make the math work.

If you choose the path of innovation, you MUST learn to monetize innovation. If you get caught into the mindset of “we’ll make money on this later” you’ll lose. If you’re on the path of innovation, you need to make money on the first unit, because you will not have the opportunity to make money on subsequent units. Getting stuck in the middle here is not an option. If you cannot make money on the first unit, then you need to learn to monetize by innovating for someone else. The idea is to innovate and pass the idea onto someone else so they can scale it. They pay for your innovation, they justify it with their forecasted returns at scale, and you move on.

I’ve met a few shops who took the innovation path. It’s a hard path. New ideas, new concepts, new things kept things fresh but it’s an intense and volatile path.

2. Sandbox Approach

The idea with this approach is to find a way of working both Focus and Innovation into your business, by cordoning off the innovation into its own sandbox of sorts. You establish a team or a division that focuses on the innovation (look up Lockheed Martin’s Skunk Works for a fun read), but you keep the innovation OUT of the operations team that is focused on scale and delivery of your core product or service.

It’s an attractive idea, to get the best of both, but taking this approach is considerably harder than it first appears and it’s riddled with risks.

One issue with this approach is that it requires serious scale in order for the operations and scaling team to produce sufficient profit and free cash flow to fund the R&D and innovation. Most of our clients simply do not have a large enough scale for this to work well.

In response to this, some of our clients try a shared resource model, which requires the sharing of resources and people across the innovation/R&D and operations/scale sides of the house. Again, an attractive idea, but in reality, it usually ends up just expanding the size of the sandbox into the yard, spreading sand thinly everywhere and creating a mess. In reality, we find that teammates are hardwired for innovation OR scale, but not usually both. So you end up sharing resources back and forth and resulting in subpar scaling/operations AND subpar innovation.

The next issue that arises is a murky financial picture. The administrative burden and efforts required for clean and accurate financial reporting of the two functions using the same resources is a mess. You can manage this a bit by using a robust time tracking system for ad-hoc reporting, but taking that data and incorporating it into the financials requires splitting payroll or allocating labor into various buckets, and trust us when we say it is not as easy as it sounds. Also, the temptation to ‘hide’ unproductive labor in the R&D buckets becomes very real and the reported R&D costs become overstated and bloated. At best you can handle the time tracking, accounting, and reporting, but your financials have an asterisk over them like Roger Maris’ 1961 homer record (the first and last sports reference you’ll hear from me this year) and any potential buyer questions the validity of the reporting.

The last issue with the Sandbox approach is managing the culture between the two teams, which at best is slightly awkward and at worst rears its head as resentment. The scalers resent the innovators because they suck up the profit and cash and the innovators resent the scalers for holding them back.

If you’re going to try this approach, despite these risks, put in place tight controls on WHO can play in both the sandbox and who focuses on the core of your business. Put in place the systems and processes to segment and account for costs appropriately. Resist and fight the temptation of hiding unproductive labor. And mitigate that asterisk over your financials by having a clean and clear narrative memorized.

3. Periodic or Seasonal Approaches

The idea behind this approach is to choose one path, say Focus, for a period of time, likely a few years, and then move towards a period of Innovation, probably a shorter time period, then transition out of the innovation period and focus again on scaling and building the innovation. This should look and feel a lot like how small innovations are made in manufacturing. You implement a change, it takes a while for the new process to be established, once it’s established, you drive the efficiency gains until the improvements decline, and you look for another change.

Again, at first glance this sounds like a great approach. You can have it all, just not all at once. Sounds reasonable. And frankly, this was probably the path that Jack and I liked the most. It had issues, but they were manageable. One issue was the same resource issue we mentioned above. Those that are hardwired for one path are likely not able to easily transition to the other. If you approach focus and innovation as seasons, you have to find a way to transition your resources during the seasonal shift.

One way to mitigate this is to pull in the innovation-focused resources as supplemental, during the period of innovation. Those resources come in the form of ‘consultants’ or ‘advisors’ but that approach can work well and allows for a combination of the Periodic Approach with the Sandbox Approach.

4. Acquistion Approach

One last approach to consider is the idea of using acquisitions for innovation. This approach requires that your business functions to scale, not innovate. Said another way, you’ve chosen for your firm the path of monogamy from an operational perspective, and you buy innovation in the form of an acquisition of IP, assets, or more likely an earlier stage operating business.

Large pharmaceuticals and medtech firms have become very good at this approach. Big pharma has moved towards this model because of the risk profile of innovation. They found that it was cheaper to simply wait for others to innovate, prove efficacy, then scoop up the firms or IP at what look like ridiculously high valuations, because this approach is cheaper than failed R&D within the firm.

The benefit of this approach is that it eliminates the high risk of failure on early-stage concepts. Additionally, this approach is faster at getting something spun up than starting from scratch, because you can buy a product or service after productmarket fit has been established.

So what’s the downside with this approach? The first problem is that it is expensive. But this can be controlled for or rather explained/justified/rationalized via the purchase price and the return on the investment. Simply account for the transaction costs and ensure the acquisition still pencils.

A bigger issue, from my perspective, is integration and culture. If your firm is built for scaling, and you acquire firms built for innovation, the integration of the innovation-focused firm into your focus-based firm is not going to be easy. I’d go so far as to say it’s doomed from the start. The key here is to know this up front, and build within the investment profile the need to turn over large portions of the existing team to scale the innovative product or service from the target firm.

Another risk to consider, I’ve never seen a product or service that were as far along in the productmarket fit as was advertised, meaning you need to be careful not to buy what you think is a product or service with an established product-market fit, only to find out that you’re still in the latter stages of development. Nothing will kill the return on an acquisition quite like purchasing what you think is a scalable product or service only to find out that you as the focused scaler now have to complete the innovation of the prior, now exited, firm. It’s a recipe for disaster.

Conclusion?

As much as we typically try to bring new levels of clarity in these letters, we have to admit this one’s just tough. We wish we had a playbook for you, but we don’t. There are no silver bullets or “goldilocks” solutions. Just self-knowledge and better-informed decisions.

Inside Ballast, we’re still figuring it out. Every time I get excited about a new idea, Jack reminds me to let the machine run. We’re both right, in different ways. If you are a business owner or leader you already know that it’s never a clean choice – it’s a balancing act. And most of the time, the best we can do is make the tradeoffs on purpose instead of tripping over them by accident.

So, all of this is to say, if you’re in this tension, you’re not doing it wrong.

See you out there in the dust up.

Thanks again to Kyle Benusa of Ballast Consulting Group for providing this letter for our blog. To read more from Kyle and his team, and to learn more about Ballast, please visit ballastconsultinggroup.com.

How VACEOs Members Are Leveraging AI Tools Today

Two dozen VACEOs members convened in late June to share with one another how they are using generative artificial intelligence (GAI) tools in their businesses. Here’s what we learned.

There are three primary ways these small business owners are using GAI tools.

- To do stuff for me – create a blog, a policy, an image, or a social media post

- To educate me – gather information on a specific interest, help me understand something

- To inspire me – the ultimate brainstorm starter to get the ideas flowing

And, what these entrepreneurs said is that it all comes down to the prompts. Get better at the prompts you give GAI, and you will get better results. They said:

- Give background and context in your prompt.

- Give as many details as possible.

- Keep asking to get to a better response. Each follow-on prompt is taken in the context of the previous prompts.

Finally, we had ChatGPT summarize the transcript of the conversation. Here you go!

They mention using it for various purposes such as creating job descriptions, drafting policies, generating marketing content, transcribing meetings, and even generating images. They highlight the convenience and time-saving aspects of the tool. The participants also discuss potential future applications, such as summarizing recorded calls, generating email responses, and creating executive compensation benchmarking reports. Overall, they express positive experiences with chat GPT and its potential for various business and personal use cases.

Meeting transcript summarized by ChatGPT

Many thanks to board member Chris Leone for facilitating this conversation.

VACEOs members can access the recording of this 60-minute Zoom meeting at VACEOs Connect. Look for Quick Links on the bottom right, and go to “Download Event Replays.”

Additionally, several members have formed a new community on VACEOs Connect for those who are active users of GAI to share their experiences with one another. Contact us if you would like to join this group.

AI-Powered Automation to Transform Finance, HR, and Sales

With every prompt you put into ChatGPT or another of the large-language artificial intelligence models producing so much buzz lately, you’re powering forward the next incredible shift in modern business operations.

These shifts began with the personal computer, which boosted output and made business fundamentals easier to accomplish. Then the Internet connected and accelerated everything. And now, AI, as it intersects with process automation, promises to deliver unprecedented new efficiencies across core functions.

The benefits will be immense, enabling organizations to achieve higher levels of productivity, accuracy, and strategic decision-making.

To better understand what’s coming down the pike, I asked colleagues at Fahrenheit (and also ChatGPT!) about what CEOs can expect as AI and automation integrate with finance, HR, and sales departments.

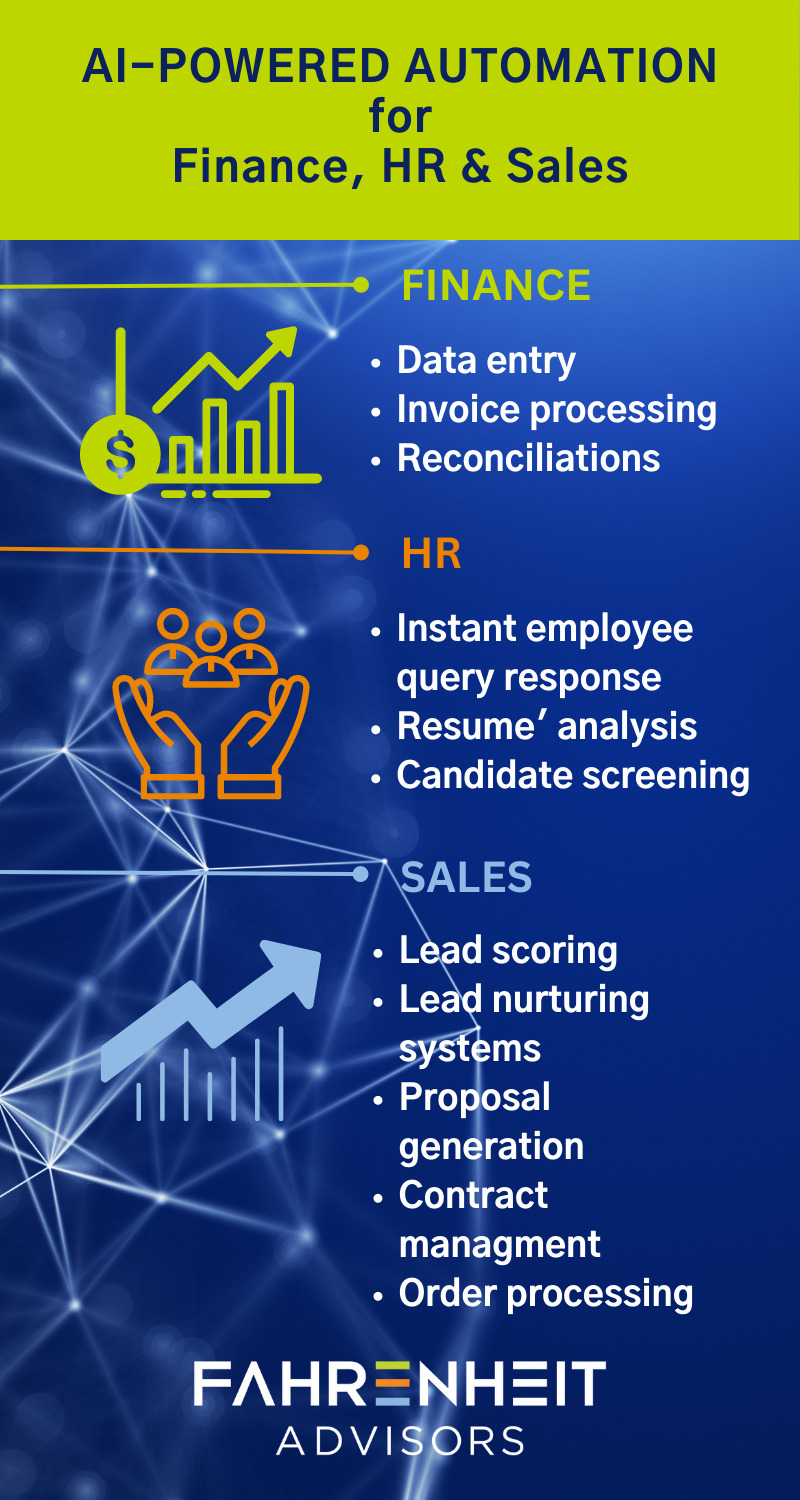

Finance: Unlocking Efficiency and Accuracy

Automation tools can revolutionize finance functions by reducing manual tasks, minimizing errors, and improving overall efficiency. Tasks such as data entry, invoice processing, and reconciliations can be automated, freeing up valuable time for finance professionals to focus on strategic activities.

Automation in finance also enhances accuracy and compliance. AI algorithms can analyze vast amounts of data, identify patterns, and detect anomalies, reducing the risk of fraudulent activities. With real-time insights provided by automation, financial decision-makers can make informed choices, improve forecasting accuracy, and identify cost-saving opportunities.

“Automation, AI, and algorithms may sound daunting to mid-market or small business CEOs, but they shouldn’t,” said Mark Vita, Business Advisory and Finance & Accounting practice leader for Fahrenheit Advisors. “Often the software and technology you already use can be configured to automate processes, analyze data, and deliver strategic insights for faster work and better decision making, and it’s just going to get better.”

HR: Empowering the Workforce and HR Pros

Human resources departments manage an organization’s most valuable asset: its people. Automation in HR streamlines administrative tasks, allowing HR professionals to focus on strategic initiatives like talent acquisition, talent development, and employee engagement. Automating tasks such as employee onboarding, leave management, and performance evaluations enhances the employee experience and frees up time for HR teams to engage with employees on a more personal level.

AI-powered chatbots and virtual assistants can respond instantly to employee queries, delivering personalized assistance and reducing the need for human intervention. Additionally, automation can improve recruitment processes by analyzing resumes, screening candidates, and identifying the best matches, leading to more efficient and effective talent acquisition.

“CEOs should not overlook the value of automation to the HR team,” said Laura Bowser, Human Capital practice leader for Fahrenheit Advisors. “The pandemic-driven changes in the workforce and workplace will continue to drive new trends, regulations, and policies that will need the HR team’s full attention. AI and automation will help them give it.”

Sales: Enhancing Productivity and Customer Experience

Automation significantly enhances a sales team’s productivity and contributes to delivering exceptional customer experiences. CRM (Customer Relationship Management) systems powered by AI can provide valuable insights into customer behavior, preferences, and purchase patterns, enabling sales teams to tailor their strategies and offerings accordingly.

Automated lead scoring and nurturing systems also can analyze customer interactions and engagement data to identify high-potential leads and guide sales representatives on the best approach to engage with them. Automation also can streamline the sales process by automating repetitive tasks, such as proposal generation, contract management, and order processing, enabling salespeople to focus on building relationships and closing deals.

“Taking a business to the next level requires accelerating and increasing sales,” said John Atkinson, Sales Advisory practice leader for Fahrenheit Advisors. “Small investments in automation tools can deliver major returns as sales teams benefit from sharper strategies and more efficient processes.”

The Road Ahead Isn’t Scary — Unless Competitors Run it Faster

AI is not a replacement for human intelligence but a powerful tool that complements and augments human capabilities. This article is proof. Feeding the right prompts into ChatGPT automatically generated a framework and usable copy in seconds, allowing me to focus on editing, fact-checking, and fine-tuning the key message I want to share.

And that message is this: for finance, HR, and sales departments, automation frees human potential from mundane and repetitive tasks, empowering professionals to leverage their skills, expertise, and creativity to drive innovation and strategic decision-making.

Implementing AI and automation must be accompanied by robust data governance and ethical frameworks to ensure transparency, privacy, and security. And businesses need to prioritize reskilling and upskilling their workforce to adapt to the changing landscape, fostering a culture that embraces technology as an enabler rather than a threat.

Those that do embrace AI and automation will enjoy operational efficiencies that drive growth and protect against setbacks. Those that don’t will find themselves running faster and faster to chase competitors.

Rich Reinecke is co-founder of Fahrenheit Advisors, a Richmond-based business advisory firm.

Productivity for SMB CEOs

Apps, processes, discipline, and little orange books.

We recently had an online “Square Table” gathering of VA Council of CEOs members to learn from one another on how to be more productive in our work and lives. Here are some of the ideas and tools that work for these entrepreneurs, business owners, and CEOs.

Email, the bane of our existence

- Inbox Zero is possible, and at least one or two of the CEOs in meeting do it daily. Here’s how, from Ari Meisel, who spoke at our Spring Retreat a few years ago. Basically, you make a decision on every email the first time you look at it — DO, DEFER, DELEGATE, or DELETE.

- One person uses four email addresses. They help him separate out personal, business internal, business external, and marketing.

- Unroll.me is a tool used by some. Some email clients have unsubscribe functions that are easy to use. Just don’t unsubcribe from VACEOs mail!

- Many folks use filters and rules to automatically move emails to folders. For example, I have a filter I use to move all email from speakers and meeting venues (it’s a lot) to a folder for later review.

- Some use Slack or Teams for internal communication, reducing email volume.

Mind Like Water . . .

- David Allen, author of Getting Things Done, talks about Mind Like Water, and defines it as “a mental and emotional state in which your head is clear, able to create and respond freely, unencumbered with distractions and split focus.” Achieving that is the trick! Following are several tricks mentioned by this group of CEOs.

- Block your time. Mark out time on your calendar for one thing without distraction – reading, writing, meeting prep, yoga, whatever.

- You brain is not good at storing information. It is made for processing. So, do whatever you can to get information offloaded and stored elsewhere. Evernote and OneNote make it easy to organize notes, store documents and set reminders.

- Use Hey Siri! or Hey Google! and tell them to remind you when you need to know.

- Some CEOs, even those who have small organizations, make use of an assistant – either someone in their business or a virtual assistant.

- Several people mentioned using journal books – the orange VACEOs books are a favorite. Some use them just for notes, others use them to list that day’s to-do list. I use a Full Focus Planner, which helps me organize my day’s work without digital distraction.

- Ari Meisel introduced me to FollowUpThen, which allows you to bcc an email and have it return to my inbox at a certain time. Gmail has similar functionality built in.

Is your time worth more than $15 an hour?

- Meetings Suck! And they waste a ton of time, as Cameron Herold taught VACEOs members a few year ago. A key takeaway — No Agenda, No Attenda!

- Calendly save you hours of back and forth trying to schedule meetings. Just send someone your Calendly link and let them choose from among available times.

- Have you (the business owner) ever spent an hour or more searching for the best deal and route for a $350 flight? Old school tip — use a travel agent. The do the searching, present you the options, and when your get stuck in Denver, you have someone to call who can actually help you get another flight. The cost is minimal.

- Finally, one CEO said that she regularly stops and asks herself, “Why am I doing this $15 an hour work? Shouldn’t I be spending my time on $1,000+ an hour work?”

What are your favorite productivity tools, hacks, and tips? Share in the comments!

4 Tips to Help Introverted Leaders Succeed in the Workplace

It is widely believed in Western culture that to be a great leader you should be an extrovert. “You need to be able to walk in front of a microphone in front of a big group, capture the crowd and be charismatic be outgoing. Think politicians, kissing babies. And that is far from the truth, explains Brad Eure, co-founder of Eure Consulting. Adding, “There are a lot of strengths that extroverts have. There are just as many that introverts have.“

According to Eure, introverts make up nearly half the population. If you think you are an introvert, you are far from being alone.

Introverts: Why the Bad Wrap?

A hundred years ago, Carl Jung defined a person as being either introverted or extroverted by how they process the world around themselves and how they get and spend energy. There are varying degrees of each, and a person can be considered an ambivert, but to simplify it: extroverts seek out and get energy and stimulation from their outside environment. It energizes them. Introverts are the opposite.

For many introverts, quarantine life today is a little easier, as most of the mixing and mingling and interruptions they encountered pre-pandemic has come to a standstill.

Introverts are sometimes stereotyped as “anti-social” or “shy”, but those traits are found in extroverts as well. “Being shy is social anxiety and it affects both introverts and extroverts,” says Eure.

“Introversion is not anti-social, is not “curable” because it is not a disease. It isn’t a choice. It is not right. It’s not wrong. It is just who you are. And it doesn’t disqualify you from being a good leader. We have found that introverts are phenomenal leaders. All of us have our strengths and all of us have our weaknesses,” he adds.

Quiet, Introvert in the House

Do you find that you often need to retreat to a quiet space to concentrate, reflect, or rest? You don’t like to rush decisions, are comfortable when alone, and prefer to write rather than talk?

If some of these traits sound like you, congratulations! You are more than likely an introvert. You have a unique self-awareness. Use that and these tips to help you be the best communicator and leader you can be.

4 Tips to Help Introverts Manage Themselves, Meetings, and Others*

#1) Own who you are.

Some may think extroverts are “natural” leaders but don’t try to be something you are not. Replace myths about leadership with truths. Be yourself, be authentic and be open and honest. This will build trust. Purposely surround yourself with people who complement your abilities and style.

Bonus tip: Eure suggests checking out “The Five Dysfunctions of a Team: A Leadership Fable” by Patrick Lencioni.

#2) Become adept at facilitating meetings when introverts and extroverts are together.

Eure reports that extroverts often dominate meetings and speak without thinking. They think passion/words/volume proves their arguments. Facilitate meetings with that in mind. Ask questions and speak up last. Draw out comments from other introverts and let them know ahead of time that you will seek their input. Like you, they want to have time to think about how they will answer.

Bonus tip: Set ground rules or Rules of Engagement for your meetings to ensure a safe space.

#3) Clearly define roles, expectations, values, and processes.

The best way to manage introverts and extroverts is by clearly defining roles, expectations, and core values. Schedule regular feedback sessions that are clear, consistent, caring, candid, and challenging. Create and strictly follow processes for everyone. Understand extrovert traits so that you are not put off by them and can lead them in the most effective way.

Bonus tip: Eure likes the Radical Candor approach.

#4) Understand the dynamics of communicating with an extroverted salesperson.

Eure reports that extroverts, especially salespersons, need to understand how their actions affect others. Keep in mind they can have sporadic listening skills. Document conversation details when appropriate and have them commit to modes of action and hold them accountable. Be able to read the body language for approval or disapproval, and praise them for their achievements.

Measurement is Key for Continued Development

Many CEOs find that hiring a consulting firm to assess their team’s personal behavior styles can be a gateway toward a strong team dynamic. While you are at it, consider engaging that firm to help establish your company’s own set of Meeting Rules of Engagement — one that balances the needs of extroverts and introverts alike.

Heartfelt thanks to Brad and Clay Eure of Eure Consulting for their assistance with this article.

*Source: “How to Lead As An Introvert”, 2021 presentation by Brad and Clay Eure, Eure Consulting.

Recent Comments